MR. ANTHONY FOK

Featured on The Sunday Times newspapers as one of the five ‘most-sought-after’ Super Tutors in Singapore

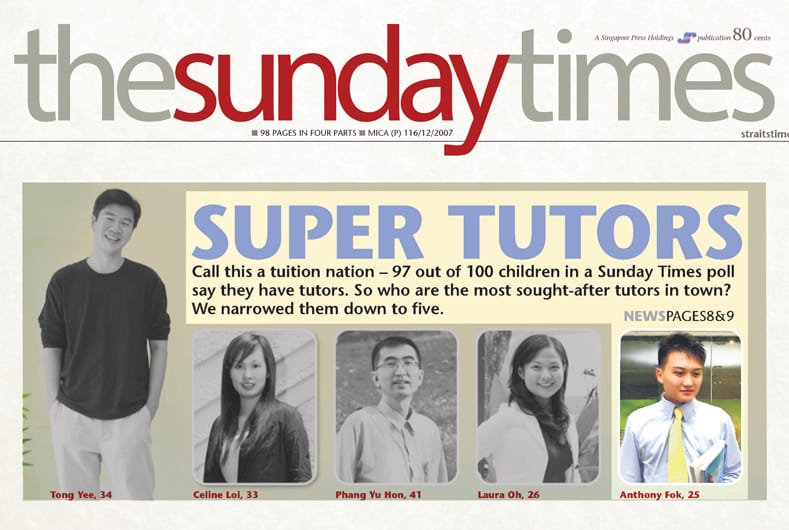

Featured on The Sunday Times newspapers as one of the five ‘most-sought-after’ Super Tutors in Singapore

Mr. Anthony Fok stands out as a leading JC Economics tutor in Singapore. Featured as one of the top five “Super Tutors” by The Sunday Times, he is known for his exceptional teaching skills, helping countless students excel in their A-level Economics exams.

Top-Rated Economics Tutor:

With over a decade of experience, Mr. Fok is renowned for his deep knowledge and commitment to student success.

Proven Track Record:

Many students have achieved outstanding results under his guidance.

Interactive Teaching Approach:

Mr. Fok makes learning engaging and simplifies complex economics concepts, making it easier for students to grasp.

Personalized Attention:

Every student receives customized lessons tailored to their learning style, strengths, and weaknesses, ensuring accelerated progress.

At JC Economics Tuition, the focus is not only on mastering economic theories but also on exam strategies. Mr. Fok equips students with the skills to analyze key economic trends, apply models, and confidently approach timed tests. His personalized approach ensures students stay motivated and excel in their studies.

Key Features:

Mr. Fok simplifies challenging economic theories, ensuring that students can apply them in real-world scenarios. His use of case studies enhances critical thinking and prepares students for both exams and future economic challenges.

“Mr. Fok’s expert guidance helped me understand tough economic concepts and ace my exams.”

JC Economics – weekly Economics Tuition lessons give students ample revision and techniques on answering case studies and essays. Detailed notes and essay structures are given for students to gain a better grasp of examination requirements. Students will also gain real-world knowledge via news articles so that they can apply their content knowledge to answer examination questions on these issues.

The Economics Intensive Revision Programme is organized for JC 1 students moving on to JC 2 next year. The lessons will cover the content required in the JC 1 syllabus and help build students understanding on a topic-by-topic basis.

The Economics Case Study Skills Workshop is designed to help students develop the essential examination techniques to tackle and ace the A-level Economics case study paper.

By attending Mr Anthony Fok’s Economics Tuition classes, students will be able to see the inter-linkages between the various topics and critically analyse the examination questions.

The founder of JCEconomics.com is Mr Anthony Fok, a zealous educator who is both qualified and experienced.

He lives by the saying that “Education is not the filling of a pail, but the lighting of a fire” and hopes to inspire as many young minds as he possibly can.

All the Economics tuition lessons are also taught personally by Mr Anthony Fok.

“As he is well known for his ability to deliver results, parents try all means to put their children in his class.”

+ Students Per Year

+ Economics Books Published

Media Interviews on Tutor

% Students Scored 'A' and 'B'